Hire a real estate broker. Make sure the broker is a member of the local multiple listing service. Regardless of whether you decide to use a traditional, full-service (full commission) broker or a limited-service (discount or flat fee) broker, you need access to the multiple listing service to sell your home for the highest price in the shortest time possible.

Prepare the home for sale. Repair known defects and perform deferred maintenance. Clean and de-clutter the home. Keep your home ready to show on a moment’s notice. There are many good resources available online with helpful tips on preparing your home for sale.

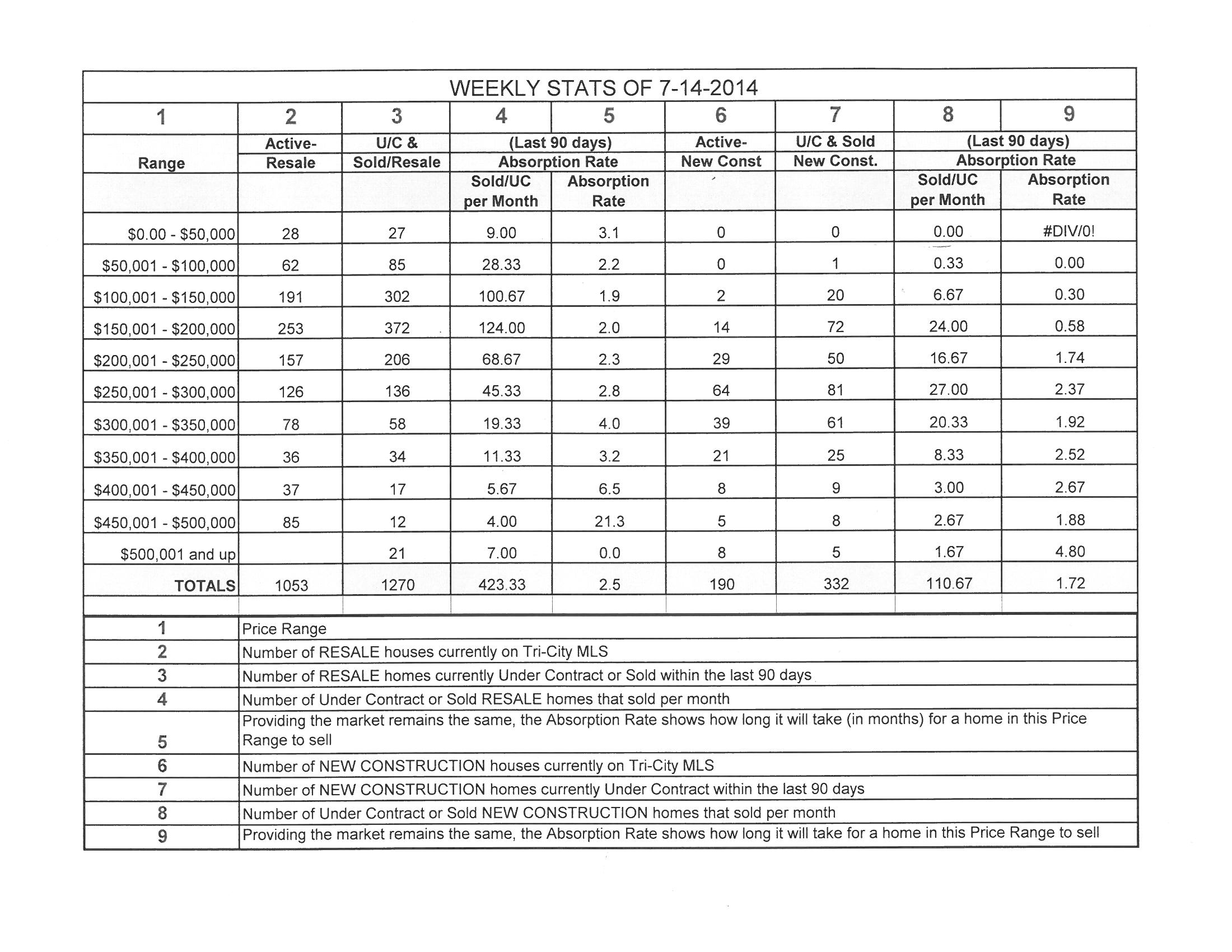

Price the home. If you hire a real estate broker, he or she will prepare a comparative market analysis [“CMA”] to assist you in pricing your home competitively. If you do not use a real estate broker, then obtain a professional appraisal from a licensed appraiser. Do not underprice or over-price your home!

Complete a Seller Disclosure Statement. In most transactions, sellers are required by law to complete and give to the buyers a Seller Disclosure Statement (known in Washington as NWMLS “Form 17”). Obtain and complete the Form 17 before have a buyer, so you will be ready!

Complete a Lead-Based Paint Disclosure. If your home was built before 1978, the law requires you to complete a Lead-Based Paint Disclosure (NWMLS Form 22J).

Get the legal description for your property. The purchase and sale agreement must contain a legal description in order to be fully enforceable, so have the legal description ready to attach to the contract. You can get the legal description from the deed you got when you bought the property, county records or a title insurance company.

Market the home. If you hire a real estate broker, marketing is his or her job! But, if you do not use a real estate broker, be sure to promote your home on the internet (including Craigslist and social media networks), as the vast majority of home buyers start their home search online, as well as through traditional methods, such as “for sale” signs, open houses, print advertisements, flyers, and word-of-mouth. Use video clips and lots of photos! Review resources on the internet for tips on creating effective advertisements and flyers.

Require buyers to be pre-approved for financing. When buyers express interest in your home, let them or their agent know that you will require buyers to be pre-approved for financing at the time of their offer.

Offer a selling broker’s commission. Usually, the buyers will be represented by their own agent. Even if you decide not to list your home with a real estate broker, offer a reasonable selling commission to the buyers’ agent. It is customary for sellers to pay commissions, so you should take that into account when pricing the home initially. Buyers pay all costs anyway regardless of whether they are “buyer’s closing costs” (in addition to the price) or “seller’s closing costs” (included in the price). If you refuse to pay a selling commission to brokers representing the buyers, you could severely reduce your chances of selling.

Negotiate the contract. When buyers decide to buy your home, they typically will make a written offer, in the form of a “Purchase and Sale Agreement.” If the buyers are represented by their own agent, the agent will prepare the agreement. You should have a real estate attorney review the offer either before signing it or include in the agreement a provision that gives you the right to withdraw from the transaction within an agreed time period, so you can seek legal advice. If neither you nor the buyers have agents, then you should have your attorney prepare the agreement.

Close the deal. Cooperate with the buyers’ agent, inspector, appraiser, title company and closing agent and make sure they know how to contact you. Customarily, the buyers will pay for their own inspection and appraisal, sellers pay for title insurance and the parties split the escrow fee. Buyers pay for financing costs and sellers pay real estate excise tax. If the transaction will be a short sale and you are not working with a real estate broker who will deal with your lender(s), consider hiring a short sale negotiator. Refer to the Short Sale Seller Advisory published jointly by the Department of Financial Institutions and Department of Licensing for important information.

Douglas S. Tingvall Attorney at Law 8310 154th Ave SE Newcastle WA 98059-9222 425-255-9500/Fax 425-255-9964 RE-LAW@comcast.net www.RE-LAW.com

This article contains general information only, and should not be used or relied upon as a substitute for competent legal advice in specific situations.

RE LAW Bulletin No. 045 Page 1 of 2 Revised 11/25/12